Transition Finance Weekly - May 8, 2026

Election Season is Here; New Insurance Data; Virginia Transmission Falls Short

BREAKING:

A week after Congressional Democrats opened an inquiry into the Trump Administration’s billion-dollar taxpayer deal to cancel wind projects, as Americans are increasingly feeling the price of electricity, New York State’s largest pension fund has asked, as an investor, if the company is jettisoning value and harming their business.

1. Utilities Spend Big Against Steyer

California gubernatorial candidate Tom Steyer has become a target of major utilities in the election, and other election updates.

California utility PG&E, the largest in the state, is injecting $10 million into anti-Tom Steyer super PACs alongside the real estate and construction industries. Steyer is a leading candidate and has the backing of environmental and climate advocates.

Steyer has a long record on climate change: he led the campaign for Prop. 39, which closed a tax loophole for oil companies to fund schools. He also founded Galvanize Climate Solutions, a climate-centered investment firm, and NextGen America, a progressive organization that began as climate-focused and been run one of the largest youth voter registration drives in history. He’s also made climate change and energy affordability central to his campaign, including pledging to significantly expand clean energy and lowering guaranteed rates of return for utilities.

Meanwhile, on Tuesday, voters in Ohio went to the polls to vote for the nominees in their gubernatorial race. Vivek Ramaswamy, former presidential candidate and anti-ESG campaigner, won the Republican nomination. Finally, voters in a hyper-rural county in Ohio narrowly upheld a ban on local solar and wind projects by a 53-47% margin.

2. Insurance Commissioners Issue New Data Call

Insurance regulators in all states are looking to better understand how climate change is impacting the insurance market.

State insurance regulators are issuing a new call for data from insurance companies, representing internal records showing losses caused by climate-driven perils in each ZIP code in which they sell policies. The call is being overseen by the National Association of Insurance Commissioners, which supports the country’s insurance regulators.

This is the first data call since 2024, in which the Treasury Department’s Federal Insurance Office collaborated with the NAIC to “better understand” climate-related impacts on insurance markets. The new data call seeks to capture a larger share of the regulated market nationwide.

Data quality remains a significant gap in efforts to assess and reform the country’s decentralized and distributed insurance industry as climate change continues to increase physical and financial risk across the country.

Jordan Haedtler, climate finance policy lead at Climate Cabinet, said,

“We literally don’t have a full and comprehensive system for monitoring insurance market data. There’s so much salience on this issue that [insurance] departments of various ideological leanings are at least finding data collection to be in their interests.”

3. West Coast Energy Market Goes Live

On May 1, a new Western energy market turned on, linking utilities across multiple states.

On Friday, a group of California utilities joined with Oregon’s second-largest utility to officially launch CAISO’s extended day-ahead market (EDAM). CAISO is the grid operator for most of California and part of Nevada.

Now, CAISO will be able to freely optimize generation and transmission between Oregon-based utility PacifiCorp and California-based utilities, essentially pooling all their assets together. The move is likely to save consumers significant dollars, as one CAISO study showed the West could save up to $1.2 billion annually.

Larger markets and interregional planning make the grid better, more resilient, and more efficient. In EDAM, Oregon customers will now see the benefit of plentiful solar power and battery storage from Southern California, while Southern California customers will see the benefit of Northwestern hydropower. Organized markets let each utility tap into a much larger pool of generation capacity.

PacifiCorp’s Vice President of Energy Supply, Mike Wilding, said,

“These organized markets are the best tool that we have available to control our costs for our customers. The way they do that is they leverage larger footprints, a larger pool of generation and more transmission connectivity than PacifiCorp has on its own, which now means you can move electricity where it needs to go more effectively and more efficiently.”

4. Virginia Transmission Sets Back Renewables

Failures in Virginia’s transmission planning process have blocked multiple gigawatts-worth of renewables from adding to the grid.

Data from PJM shows that more than 100 new energy-generating facilities since 2018 have been “withdrawn or significantly delayed” by failures to upgrade existing transmission or build new transmission capacity in Virginia. Most of those have been clean energy projects.

The review of delayed and blocked projects found dozens of projects by Dominion Energy, Virginia’s largest investor-owned utility. The cancelled projects would have added 5 GW to Virginia’s grid.

Transmission remains a significant bottleneck to the energy transition, particularly as the country’s aging grid meets new large loads in data centers and struggles to handle new generation capacity in the clean energy boom. Interconnections and transmission pitfalls have long been a barrier to bringing new, much-needed clean energy online.

5. Salt River Project To Develop 3GW of Arizona Solar

The state’s largest public utility will build 3GW of new solar as a new clean energy majority takes their positions on the Board.

The Salt River Project, a public utility serving 2 million Arizonans, announced that it will partner with developer NextEra Energy Resources to develop 3 GW of new solar capacity in Arizona by 2034. The plan will add 500 MW of new solar per year from 2029 to 2034.

SRP is seeking to “double” its generating capacity as it seeks to meet rising load growth, and this addition will triple the total amount of solar it has on its grid. Around 1GW of its existing solar was also developed by NextEra.

Despite its relatively low profile, SRP saw headlines in recent months as it held elections for its board system, in which a pro-clean energy slate won an outright majority, defeating candidates backed by the far-right political group Turning Point USA.

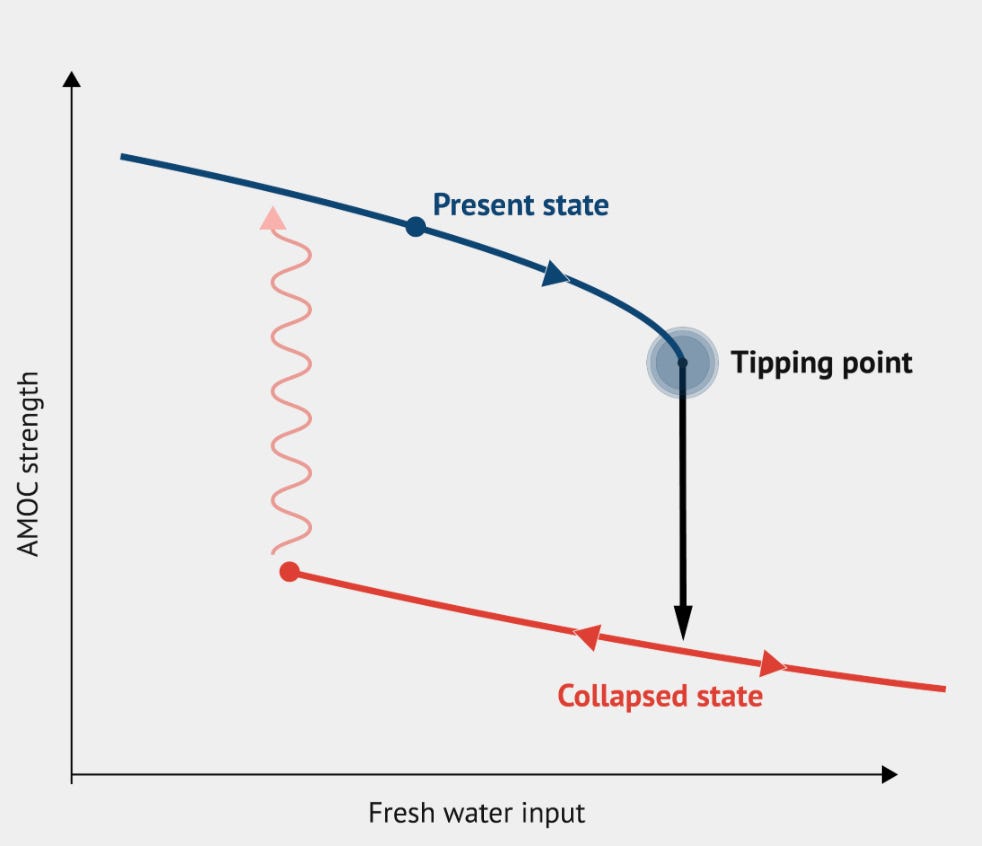

6. Tipping Points Threaten Global Stability

Climate change’s irreversible thresholds threaten fundamental global climate patterns that undergird the modern world.

As climate change brings about felt impacts via climate-driven disasters, its sub-surface impacts on global currents are becoming more clear, and worrying. Experts have identified the Atlantic Meridional Overturning Circulation (AMOC) as “under threat” from climate change as warming seas and temperatures, melting ice, and more rainfall change the balance of the North Atlantic.

The AMOC is a critical system of ocean currents, which includes the famous “Gulf Stream,” keeps much of the world as it is today: it keeps Europe warm, and cools down areas close to the equator. As climate change weakens the streams of currents, AMOC approaches a “tipping point,” in which the climate-driven changes weaken it to the point of collapse.

Countries, companies, and key decisionmakers are now having to think about these threats more clearly. In late 2025, Iceland declared the potential collapse of AMOC an “existential threat” and a key national security concern. Meanwhile, JPMorgan is responding to client interest in understanding tipping points and navigating uncertainty.

SPOTLIGHT: New Recommendations for Insurance Regulators

A new report from Brian Shearer, Director of Competition and Regulatory Policy at the Vanderbilt Policy Accelerator, argues that there’s a “greedflation” problem in insurance markets, and outlines steps that regulators and policymakers can take to address it.

The report argues that insurers are spending too little of the money made from people’s premiums on paying out claims, creating a low “loss-ratio.” A loss-ratio is the term for the proportion of premium-revenue paid as claims. The report finds that most insurers’ loss-ratios are between 50% and 70%, and have been falling for years. Shearer argues that property and casualty insurers should be held to a similar standard as health insurers, which are required under the Affordable Care Act to spend a minimum of 80% of their premiums on medical care and improving the quality of care.

This ratio matters for families as climate-related risks increase financial risks to properties. The report also argues that insurers spend too much money on unnecessary expenses, advising lawmakers to cap or prohibit insurers from spending corporate dollars on private jets, lobbying, campaigning, and excessive advertising.